Key Takeaways

- Apple will dominate thanks to brand, installed user base, and ecosystem of products

- More revenue from Services will increase gross and net margins

- Apple Silicon is paving the way for it to gain market share in the PC space

- More parts being developed in-house should increase product margins

- Biggest risks are manufacturing challenges and reliance on emerging markets growth (India)

Catalysts

Apple’s Brand leads to sticky revenues and increasing installed device base

Apple has become more than a tech hardware and software company, it has become a lifestyle product. It has embedded itself into the lives of billions of people around the world, many of whom say they couldn’t live without their iPhone. Its brand has been built up over decades, and is now a competitive advantage that allows it to maintain margins higher than peers, and generate revenue that is a lot more sticky.

When users go to upgrade their device, they’re much more likely to look within the ecosystem they’re already accustomed to, and have so much of their digital life set up on, rather than searching externally among the non-Apple options.

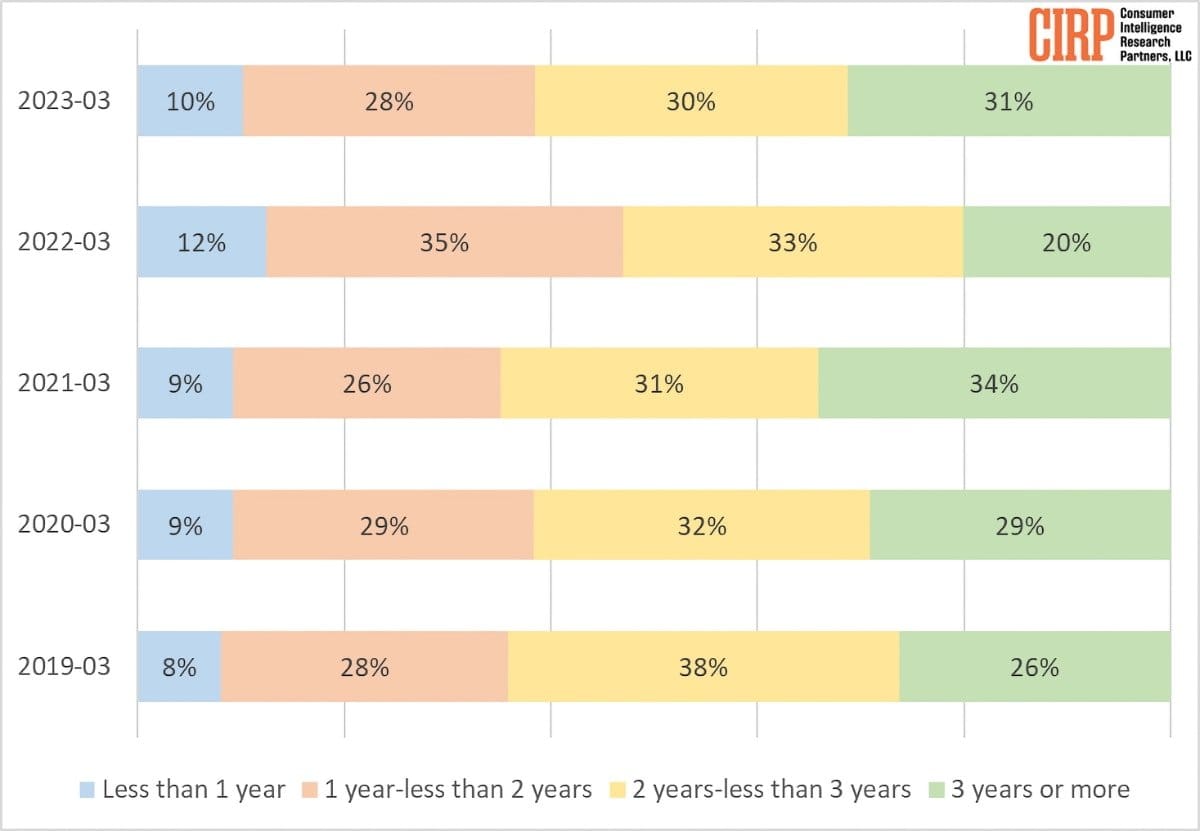

Research from Consumer Intelligence Research Partners indicates that roughly 1/3 of iPhone users upgrade their phone within 1-2 years, 1/3 upgrade within 2-3 years, and 1/3 upgrade every 3+, while only 10% upgrade every year - so it seems to be a pretty even split.

Source: Apple Insider

Considering more Americans than ever are using iPhones over Android phones, and Apple captures 49% of the global refurbished phone market in 2022, it seems like the brand reputation is stronger than ever, and will likely see its installed user base of over 2 billion active devices continue to grow.

The deeper a user goes in the Apple ecosystem, the higher their switching costs become

Since Apple's products, services and software have become instrumental in users' lives, there is now a “switching cost” for users if they choose to go to a different ecosystem. If a user becomes a heavy user and reliant on iMessage, Calendar, FaceTime, iCloud and many other services and features within the Apple ecosystem for their day to day, the process of switching to an alternative ecosystem becomes less appealing.

Source: The Product Head

And while this is just anecdotal evidence, personally I’m not keen to pay that cost so I’ll stick with Apple as long as it keeps delivering me value that outweighs the switching cost. Now I have an iPhone, 2 Macbook's (1 for work and 1 personal), a pair of Airpods and an Apple TV subscription.

The longer users are in the Apple ecosystem, and the deeper they go with services and accessories from Apple, the more they are likely to stay paying users because switching their digital lives back to Windows, Android or any other provider would be painful and cumbersome to say the least. And the unified experience among the Apple ecosystem between devices and services keeps many users satisfied.

This will help make revenues more “sticky” and predictable, and likely contribute to higher uptake of future complementary products and service releases within the Apple ecosystem, like headphones, laptops, PCs, wearables, etc.

Pricing Power will allow product revenue to grow, even if volumes don’t grow as quickly

Since the business is quite mature, I don’t expect much growth from unit volumes of its core products considering the huge size they already have. However, I do believe that with future product releases, they can incrementally increase the price as long as they continue delivering incremental value to the user, and so when users are upgrading their devices (after 1-4 years), they won’t be deterred by a slightly higher price due to the value that the devices deliver. There are plenty of reasons users are willing to pay the higher price (here’s 9).

Source: FourWeekMBA

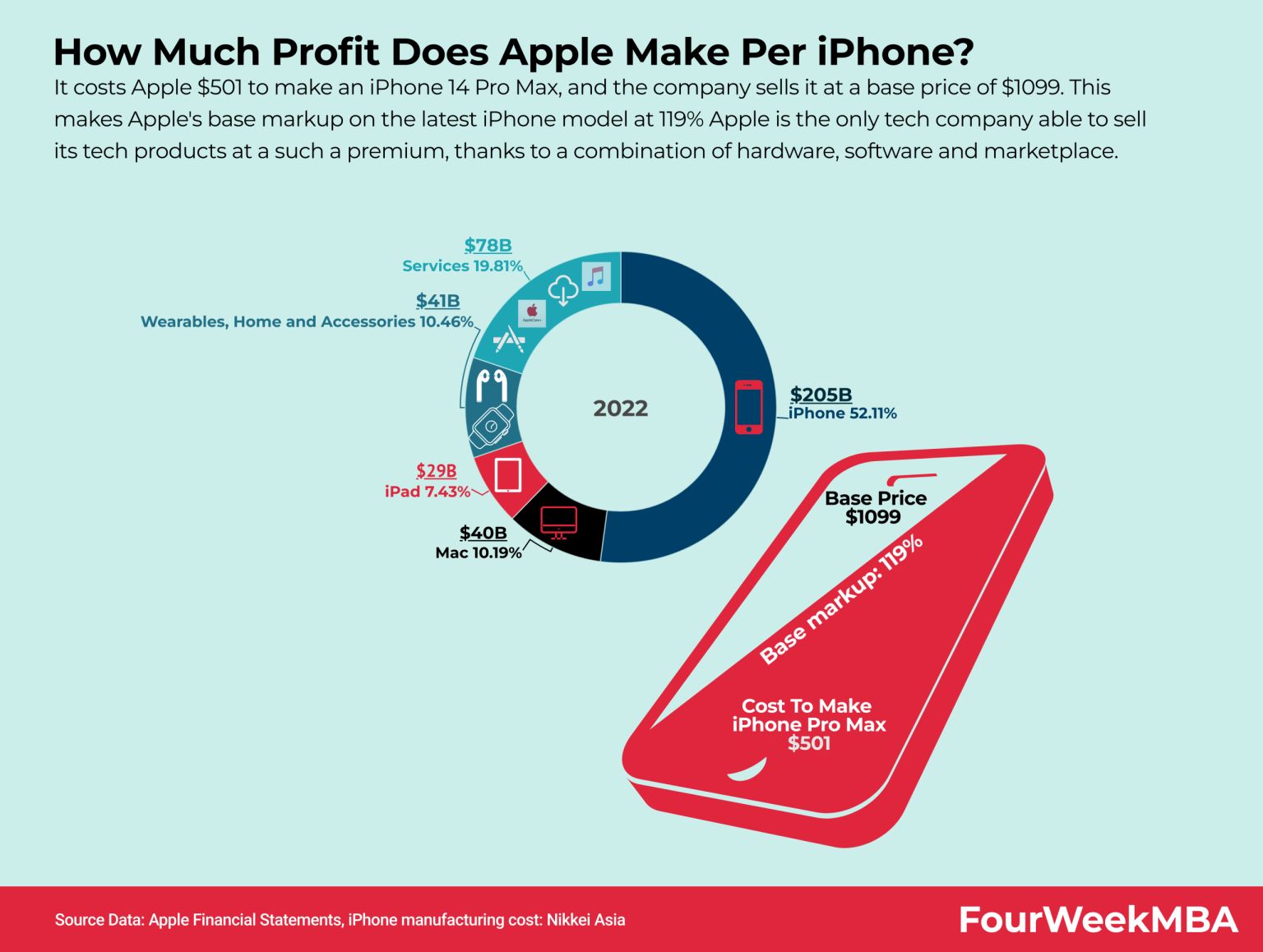

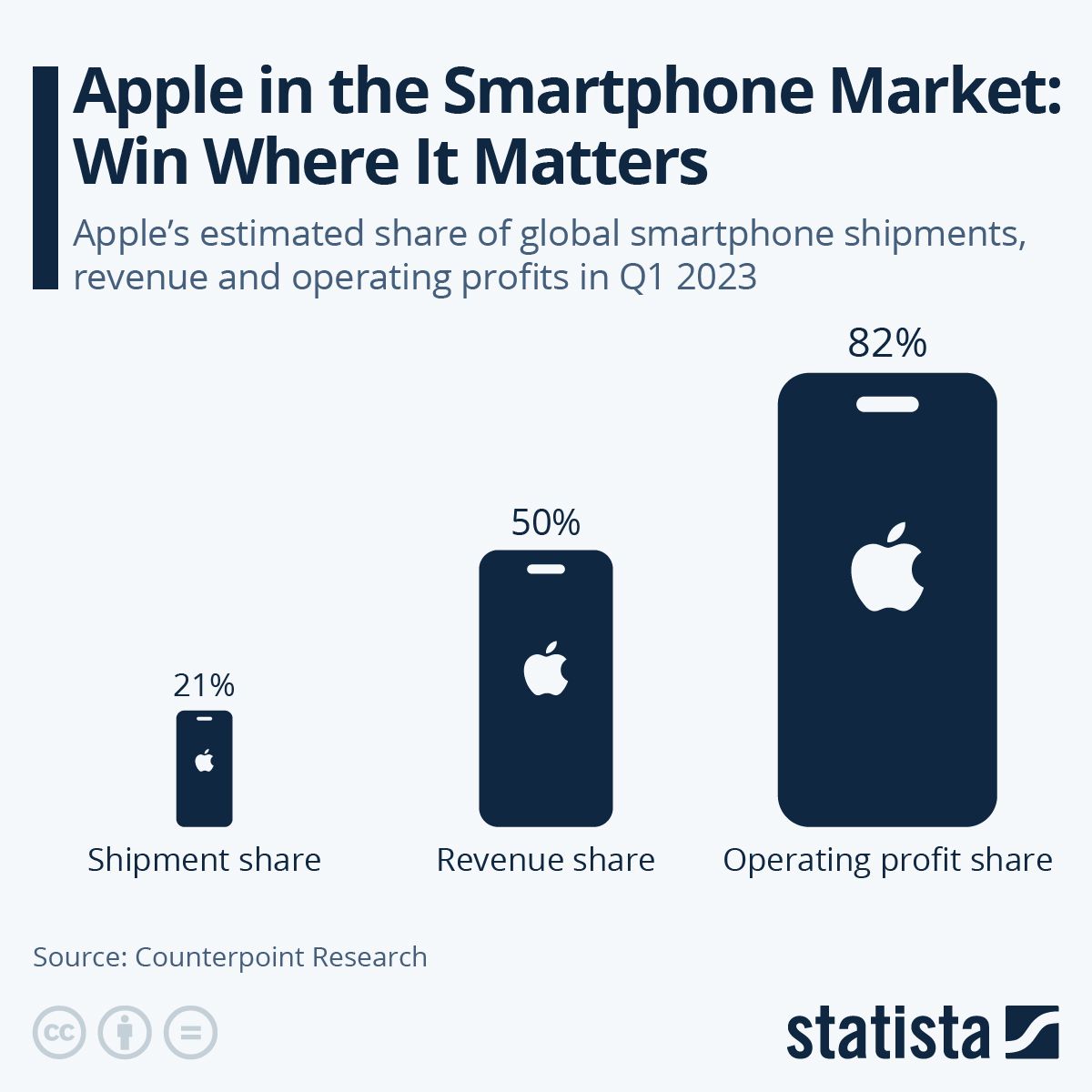

This is exemplified by the fact that Apple generates roughly 85% of all smartphone profits, and 48% of all revenues, yet only has about 24% market share. Smaller market share, yet huge profitability from better margins than competitors comes from that pricing power.

Source: Statista

Additionally, Apple’s iPhone 7 series started at $649, and 3 years later, Apple’s flagship iPhone, the 11, cost 54% more at $999, yet according to sources those phones sold in similar volumes of around 159 million units.

Product margins to increase as more parts come “in-house”

Surprisingly, Apple is now reaching a stage where it can deliver high-quality products, but without the premium price tag to peers. This applies mainly to base model devices in the different product segments, not the top tier variants.

Take for example the base model M1 chip Macbooks and iMacs, or even the iPhone SE variants, both are great examples where Apple is delivering incredible products but at equal or cheaper prices than similar products on the market.

This is because as Apple moves more processes in house like it has with the chips (and probably will in the future with other parts like screens), it’s likely we’ll see margins from product revenue improve.

Rough estimates show that the M1 chip likely costs around $40-50 per device, when the corresponding Intel Core i5 chips (x86) cost Apple around $175-200 per Dual core device, and $200-225 per Quad Core device.

While these are just estimates and not including the R&D to get there, that’s still a huge saving even if the estimates were slightly inaccurate and M1 chips were closer to say $100 per piece.

If Apple can execute the same cost reduction on other inputs into its products, which I think they can, this could help gross margins improve. If you think longer term, like Apple is, you’d be willing to make those investments for the added benefits of control, cost per unit reduction and performance increases.

It appears Apple is slowly moving away from its expensive contracts with these part providers, which will likely lead to cost reductions within the product segment, and therefore higher margins from this part of the business.

Apple’s growing and high-margin Services business could increase overall margins

For many years Apple has primarily been a product business, and I have no doubt it will continue to be.

However, slowly but surely, as more people adopted the core products of the ecosystem like iPhone's, Mac's, etc, Apple added more and more additional “services” (some free, some paid), that complimented these products and did a good job at keeping users embedded within the ecosystem. This includes the App Store, iCloud, AppleTV+, Apple Music, Apple Fitness+ and the free offerings like iMessage, FaceTime, etc.

I believe the adoption of Apple's complimentary higher margin paid “services" will continue to grow among existing users and new product users alike.

Source: FourWeekMBA

At the end of 2018, the company had an installed user base of 1.4bn (900m for iPhones), and reportedly had over 330m paid subscriptions at that time, a 23% uptake. Considering the company now has an installed user base of over 2 billion, and 935m paid subscriptions, that uptake has increased to around 46%.

So adoption of these services appears to be working and likely to continue, as long as Apple can continue to add value to users (better content on AppleTV+, more apps in the App store, better iCloud services, etc). I believe this will be the biggest contributor to revenue growth as more users in the installed base take up certain subscriptions, and existing users take up additional subscriptions, and revenue from the App Store continues.

Additionally, considering the product business is relatively mature, new product releases will likely not move the needle in a big way.

New revenue sources from future product and service releases

Some have claimed Apple’s innovative days are behind it, but I beg to differ.

When Apple creates a product, they don’t ship small and learn fast and then iterate. They have the resources internally to release a product after countless internal iterations where they eventually reach the point where their high internal standards for a product are met, and they feel confident to release it. New products can often take a while to pickup steam in terms of contributions to overall sales, but more often than not, they do eventually pickup.

The Apple Watch and AirPods are two recent examples. Released in 2015 and 2016 respectively, they reportedly sold 53 million and 82 million of these products in just 2022 alone (not including prior year sales), with those sales estimated to have brought in revenue of around $10bn for AirPods, and around $14bn-18bn for the Apple Watch (because Apple doesn’t disclose exact figures).

With that in mind, I believe Apple's R&D expenditure (7% of revenues) will lead to new products in its lineup such as the highly anticipated Vision Pro headset, Apple Car and others. Some of these new products are expected to be released within the next few years, BUT I don’t think they will contribute meaningfully to revenues until after 2028.

For example, estimates of sales of the Vision Pro headset were originally expected to sell around 1 million units in 2024 (which would’ve been about $3.5bn in revenue), but revised estimates range anywhere from 150k units, to 400k units in 2024 (which would be $525m - $1.4bn in revenue instead).

Transition to in-house silicon chips is building the moat, and taking market share.

The release of Apple Silicon chips was one of the mostly widely anticipated Mac updates in years. The company had reportedly been working on the project for about a decade. The Apple ethos of owning both the software and hardware, like it does with its iPhones and iPad’s was taken up a level when the company was willing to bet a decade’s worth of R&D to create Apple silicon chips with ARM to develop a custom 64-bit instruction set architecture (ISA) for PC’s like it has with its phones. This move allowed it to move away from Intel x86 architecture chips, and enhance the performance of its PC lineup considerably.

There are plenty of videos (1 and 2) and articles out there that explain the huge benefits and technical details of the new chips and architecture way better than I can, so I won’t go into that here. I’ll focus on the why these hardware upgrades are promising for Apple’s share of the PC market.

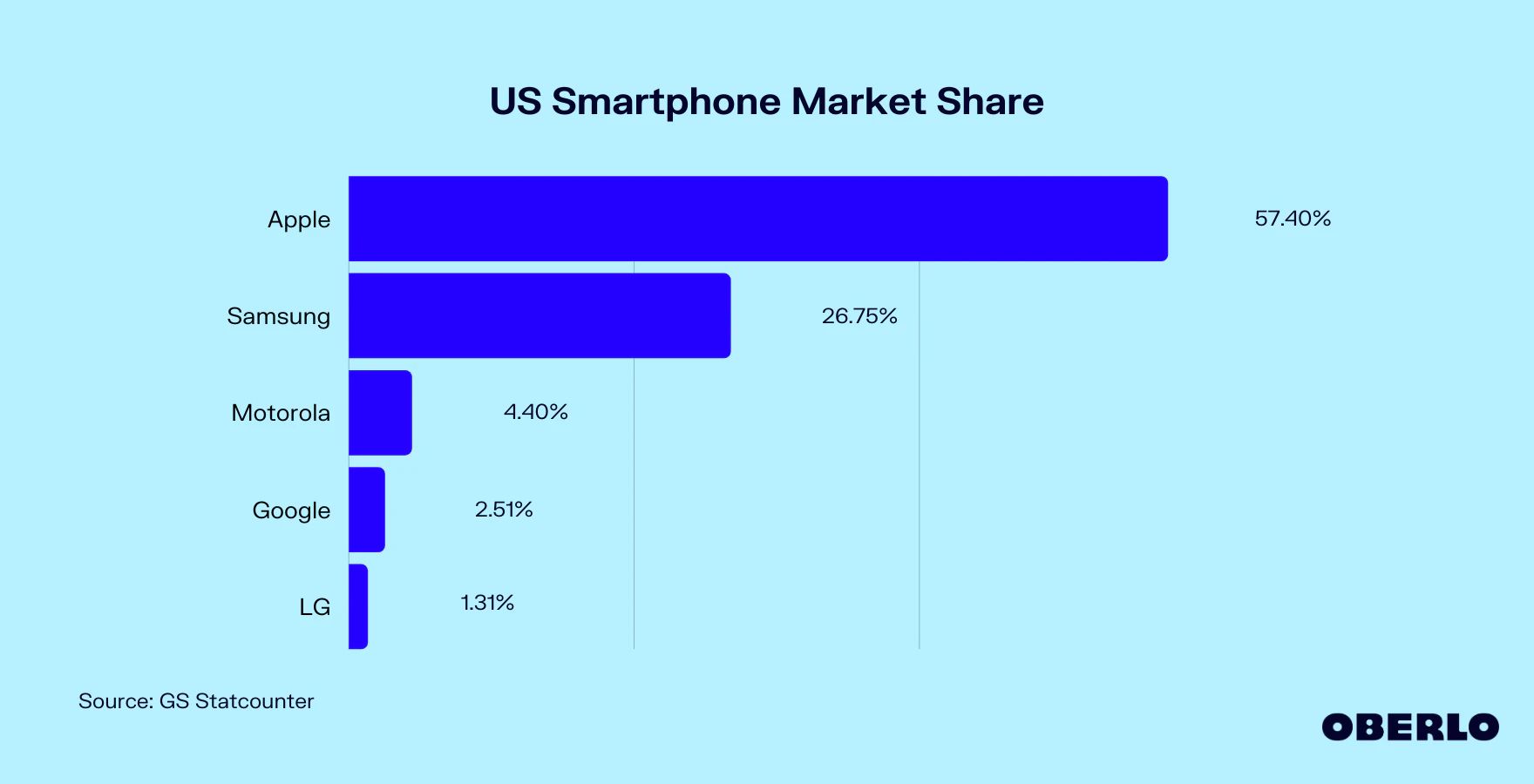

Owning the processors has allowed the company to innovate with its phones and tablets, and gain significant market share of 57% of smartphones in the US and 55% of tablets in the US.

Source: Oberlo

Now that it owns the PC processors, I believe this will likely allow it do now do the same with its PCs and help it gain market share.

Despite a weakening global PC market where the likes of Lenovo, HQ, Dell and Acer all saw year-on-year declines in shipments, Apple was the only one to record year-on-year growth in shipments, according to IDC data. It’s market share grew from 6.8% in Q2 2022 to 8.6% in Q2 of 2023.

While the Global PC market is only expected to see low growth over the next few years in terms of revenue or shipments, it’s likely that Apple’s transition to an in-house chip and future iterations on that chip will help it gain market share through providing a better PC experience that is hard to match from competitors.

So while this portion of the business is only small, I believe it will continue to gain market share in this slowly growing market thanks to increasing its market share during this decline, and then a future recovery of the PC market.

Indian expansion to help with manufacturing stability and possible sales growth.

Apple is taking a dual-pronged approach to India, where it hopes to take what it’s learned from China, and establish manufacturing in India to diversify production, as well as attempt to penetrate the local smartphone market to generate new geographic revenue streams. Apple currently only has around 3.9% of the Indian smartphone market, and is attempting to take some market share from Android's current dominance of 95% (as of 2022).

Local reports suggest that sales in the region were about $4bn USD in Fiscal 2022, and Bloomberg reported that Apple had nearly $6bn in sales for the year to March 2023. Considering those sales were without any retail presence (it only opened its first two retail stores in the country in April 2023), and the country has a massive and expanding middle class to potentially power sales growth, and support from Prime Minister Narendra Modi on the manufacturing side, the opportunity for Apple here is large enough to move the needle.

However, Apple will need to address the cost issues (with current pricing they are largely unaffordable for most local consumers compared to other cheaper Android variants), and it’ll need to delicately balance relationships with Chinese and Indian governments as it makes the transition.

As of Q4, the Indian smartphone market was reportedly 150 million units per year, and iPhones accounted for 7 million of these. Some analysts expected that the addressable market could reach 280-290 million units per year in 10-15 years, which would be on par with the Chinese market currently. If you assume Apple could eventually reach 18% market share in India like it has in China, that’d be around 50-52 million devices per year, which is 7x higher than its current 7m devices sold per year, which could roughly equal $42bn in revenue.

I don’t expect India to contribute meaningfully to revenues in the next 5 years, but it is growing quickly (now the 5th largest iPhone market overtaking France and Germany), and I do I believe it could contribute meaningfully (more than 10%) to total sales in the next 5-10+ years.

Buybacks will help drive shareholder returns.

Apple’s trend of buybacks since 2013 has reduced shares outstanding by roughly 5% per year. I believe the huge buybacks will continue, since it clearly has enough capital to fund internal operating expenses and capital expenses.

These buybacks will likely drive the majority of shareholder returns by increasing EPS, rather than any dramatic gains in company size, sales or unit volume. If there is any significant increase in product or services sales, this is a bonus, but I’m not relying on it in my valuation.

Assumptions

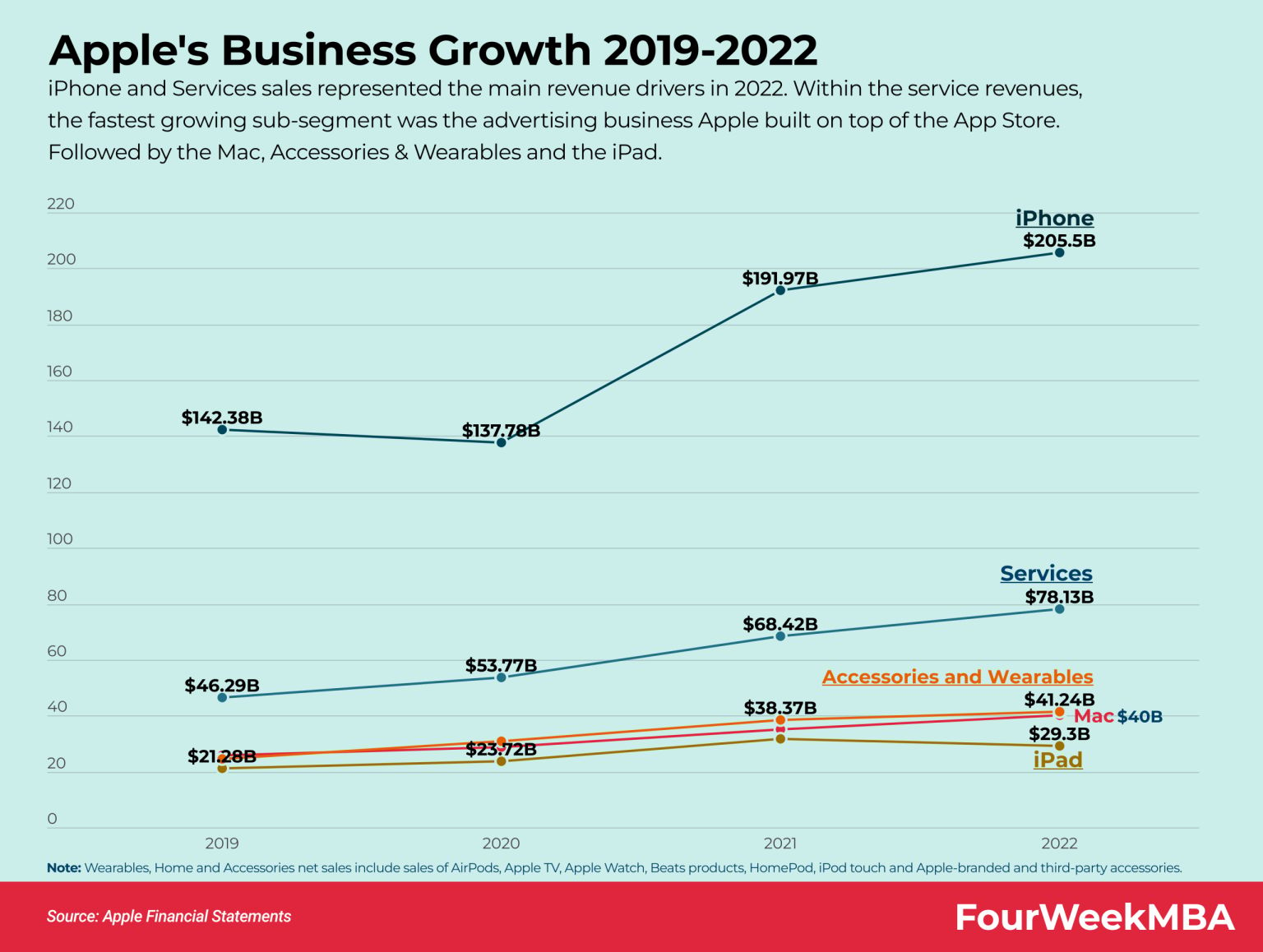

Revenue breakdown as at Q2 2023

Products - 78% of revenue

- iPhone (54% of revenue)

- Mac (7.5% of revenue)

- iPad (7% of revenue)

- Wearables, Home and Accessories (9.2% of revenue)

Services - 22% of revenue

- Advertising, Apple Care, Cloud Services, Digital Content, Payment Services.

iPhone revenues to experience low growth

I expect iPhone revenues to grow slowly at around 4% per year, to reach $257bn, up from $205bn from end of 2022. This is driven by high rates of retention from existing users through their upgrade cycle, slight market share increases in the smartphone market and slight price increases. This means iPhone would go from about 54% of revenues to 50% as other products and services experience more growth.

Mac revenues to grow steadily as market share is taken

I expect Mac revenues to grow to at about 6.5% per year to reach $55bn, up from $40bn at the end of 2022. This is driven by increases in PC market share as described above, and a recover in the PC market from its current slump. This would represent 11% of revenues, up from 7.5%.

iPad revenues to have weak growth

I expect iPad sales to grow relatively weakly at 2% per year to reach $34bn, up from $29bn at the end of 2022. This would be a result of a “structural decline” in the tablet market, and the fact that most users have a much slower replacement cycle than their iPhones. This would take the segments revenue contribution from 7.5% today to 6% in 2028.

Wearables, home and accessories revenues to grow steadily

I expect this segments growth to be stronger than the likes of the iPad segments given the Apple Watch, Airpods, Apple Home and other accessories have more compelling use cases than iPads. It will likely grow at 7% per year to reach $57bn in annual sales by 2028, up from $42bn in 2022 due to price increases, new product releases and an existing amount of users within the Apple ecosystem (from iPhones) acquiring Airpods and Apple Watches as complementary products to their main devices. This would mean it becomes 11% of revenues, from 9% today.

Product margins to increase as more components are made in house

Based on Apple’s incremental shift to more internal production of better parts for more of its products mentioned earlier (like chips, screens, modem chips, etc), I expect the company’s gross product margins to improve from 36% today, to 40% by 2028 as it relies less on expensive contracts for parts from third parties.

Services revenues to continue as adoption from installed user base continues

While the paid subscriber count has grown at around 25% per annum for the last few years, I don’t expect this to continue. Instead I assume Apple will grow paid subscribers today from 935 million to 1.5bn by 2028, a growth rate of 10% per annum due to a continuation of the increased adoption of services from its installed user base, and growing App Store revenue.

I believe the revenue from its services business will grow to $154bn, up from $83bn today, which is a 12% annual growth rate. The services business currently has 935 million subscribers that pay an average of $88 per year in for the services (This isn’t a perfect metric considering “services” is a mix of different business types like App store vs Music, etc). But with this rough metric in mind, I assume the average annual revenue per paid subscription will increase to around $100 (due to incremental price increases).

Revenue Split To Move More Towards Services

I believe its revenue mix will likely change from 80% products and 20% services (36% / 71% gross margins respectively) to a 70/30% split of products/services due to higher growth in services. I think the respective margins for each segment in 2028 will be 40% / 71%.

This will lead to gross margins of 49% (currently 44%).

Overall profit margins To Increase

I believe Apple is very diligent with its operating expenses, and will be consistent with its current expenses as a percentage of revenue. I assume Research and Development (R&D), and Selling, General and Admin (SGA) expenses will both remain about 7% of revenues respectively as that is what they have been over the last few years, and their tax rate will increase to 16% (from 14%) based on the fact that its average tax rate between 2018 and 2022 was 15.6%

With a $252bn gross profit, $36bn R&D expense, and $36bn in SGA expense, that leaves a Net profit before tax of $180. With the 16% tax rate, that means a $28.8bn tax bill, and a subsequent $151bn in net profit for that year.

So, with this in mind, and the change in revenue split, as well as the higher gross margins from products, I expect the company’s net profit margins will increase to 29% from 24.5%.

Risks

Manufacturing Risks Are The Biggest Concerns And A Delicate Balancing Act

It is no secret that Apple has a risk with it’s large exposure to China for its manufacturing needs. However, Apple has been aware of this for years and has been acting on implementing changes.

Reports indicate that Apple is aware of this too. Reuters analysis believes that in the 5 years to 2019, “China was the primary location of 44%-47% of Apple’s suppliers production sites, but that fell to 41% in 2020, and 36% in 2021”. (But Apple did not confirm).

If true, and we believe Apple makes long term moves like it does with its R&D, it seems likely that the company is actively updating its global supply chain structure to be less reliant on China.

A senior analyst at Isaiah Research told Supply Management that Apple was “looking to reduce the risk it faced from too much supplier concentration”.

Having a decentralised network of suppliers should help reduce the company’s risk in this area, but it won’t be an overnight job and will take years, but it seems like it’s already made a lot of progress.

Apple’s Deal With Google Is High Margin, But High Risk

Rumours are that Apple has a non-compete deal with Google where it uses Google as the default search engine for Safari, and in return Apple receives a portion of the search revenue generated by Chrome users on iOS. It’s believed that back in the day Google hypothesised that it was better to compensate Apple for what they could’ve earned from its own search engine than to compete with them.

Google reportedly viewed Apple creating a search engine as “Code Red” because half their business comes from iOS. While it’s difficult to get confirmation on any particular figure that is paid per year since it's obviously not disclosed, it’s estimated that it could be around $15bn per year as of 2022 and this revenue comes through the services business stream (which could possibly be 20% of services revenue).

If Anti-trust lawsuits against Google eventuate into a cancellation of the deal, it could result in a notable decline in Apple’s services revenue in the short-medium term. However, since Apple has Safari, and is building up its privacy-focused advertising business, I believe that IF the non-compete deal between these two companies was to be removed, then it would impact Apple’s Services revenue in the short term, but they’d likely pivot and invest in scaling Safari plus their own advertising business and make up the shortfall in that revenue in the medium term (5+ years time).

Failure To Gain Traction In The Services Businesses Would Weaken Profitability

There is a risk that Apple’s services businesses don’t provide enough value to incentivise existing Apple product owners to sign up to the service. We have seen Apple’s service growth slowing over the last few years, but I believe this is a temporary slowdown due to the macroeconomic environment over the last 1-2 years being one of cost cutting and reining in budgets for consumers.

Currently, Apple’s services businesses aren’t the leaders in their respective fields. Apple Arcade game pass is competing with the likes of Xbox Games Pass and Playstation Plus. Apple Music is competing with Spotify (515m Monthly active users). iCloud competes with Google Drive and Dropbox. Apple TV+ is competing with Netflix, Amazon Prime and all the other streaming services. Apple Fitness+ is competing with the likes of Nike Fit Club, Freeletics, Centr and many others. News+ is competing with many other magazine subscription services and just free news in general.

The point here is Apple’s bread and butter is tech hardware (devices) and software (iOS, macOS, etc).

These services business are all complimentary and within the software side of things, and they’ll need to invest the same, if not more than these competitors in these areas in order to maintain or steal market share. Since some of these services aren’t Apple’s core focus, they may receive less love and attention (on a relative basis) than those businesses that focus on those areas explicitly (Dropbox, Spotify, Netflix, etc), and this may result in lower than expected adoption.

How well do narratives help inform your perspective?